Key Takeaways

- Most platforms that claim white-label insurance capability deliver surface-level branding — not true partner-level customisation.

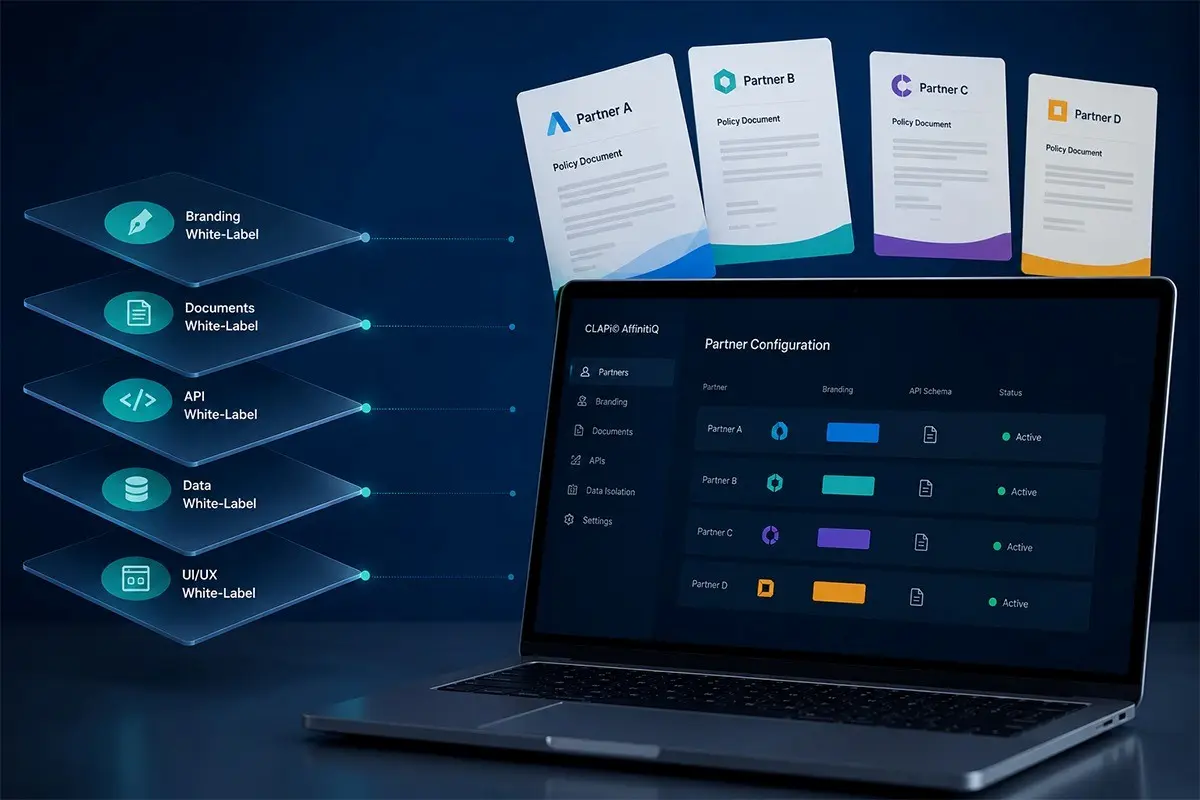

- A genuine white-label insurance platform requires configurability at five levels: UI, documents, APIs, data isolation, and compliance.

- Insurers whose distribution partners demand white-label experiences — banks, fintechs, retailers — need a platform that can deliver this without custom development per partner.

- The distinction between surface white-label and deep white-label becomes critical at scale — when an insurer is managing ten or twenty distribution partners simultaneously.

- CLAPi© AffinitiQ delivers genuine multi-level white-label capability designed for insurers managing large and growing partner portfolios.

White-label insurance is one of the fastest-growing distribution models in Asia Pacific. Banks, fintechs, e-commerce platforms, telecommunications companies, and retailers are all seeking to offer insurance products under their own brand — leveraging their existing customer relationships and digital touchpoints to distribute coverage without appearing to do so through an insurance intermediary.

For insurers, this represents a significant distribution opportunity. But realising it requires something that many insurers discover too late they do not have: a technology platform capable of delivering a genuinely white-label insurance experience at scale, across multiple distribution partners, without a custom development project for each one.

This article examines what a true white-label insurance platform must deliver — and the gap between what most platforms claim and what they actually provide.

What “White-Label” Actually Means — And What It Does Not

The term white-label is used loosely in insurance technology, often to describe capabilities that range from genuine end-to-end partner branding to little more than a logo replacement on a standard template. Before evaluating any platform’s white-label capability, insurers should be clear on what the term should mean:

- True white-label means that a distribution partner’s customers experience the insurance product entirely as the partner’s own — the insurer’s brand, name, and identity are absent from every customer touchpoint. The purchase experience, the policy certificate, the claims process, the renewal notice, and any digital interface all carry the partner’s brand exclusively.

- Surface white-label means that the partner’s logo and colour scheme are applied to standard insurer-branded templates and interfaces, but the insurer’s identity remains visible — in document footers, email sender addresses, policy wording references, or the URL of the customer portal.

The difference matters commercially. A bank distributing insurance under its own brand needs its customers to believe the product is the bank’s own. Any visible insurer branding undermines that perception and reduces the conversion and retention rates that make bancassurance and affinity distribution commercially valuable for the partner.

The Five Levels of White-Label Capability

A platform’s white-label capability can be assessed across five distinct levels. Most platforms that claim white-label capability deliver Level 1 or Level 2. A genuinely capable white label insurtech software platform must deliver all five:

-

UI and Visual Branding

The most basic level: the partner’s logo, colour scheme, typography, and visual design are applied to all customer-facing interfaces — the purchase flow, the customer portal, and any digital touchpoints. This is table stakes for any white-label claim, but it is often where platform capability ends.

-

Document and Communication Branding

Every document generated by the platform for the partner’s customers — policy certificates, welcome letters, renewal notices, claims settlement letters, premium receipts — carries the partner’s brand exclusively. Footers, sender email addresses, document metadata, and policy wording references must all be configurable at the partner level. Most platforms that fail at this level do so because their document generation system uses shared templates with hard-coded insurer references.

-

API-Level Brand Isolation

When the distribution partner’s system calls the insurer’s platform API, the response data must be free of insurer-specific references that could surface in the partner’s customer interface. API responses that include insurer company names, system identifiers, or branded field names create a technical white-label failure even when the UI and documents appear correctly branded. Branded insurance portal technology at the API level requires the platform to expose partner-specific data schemas rather than insurer-centric ones.

-

Data Isolation Per Partner

Each distribution partner’s customer data — policyholder records, claims data, premium history — must be fully isolated from other partners’ data within the platform. This is not just a security requirement (though it is that) — it is a contractual requirement of most distribution partnerships. Partners need assurance that their customer data is not accessible to other distribution partners on the same platform, and that data residency requirements applicable to their customer base are met.

-

Compliance and Regulatory Persona

In many APAC markets, regulatory requirements impose specific disclosure and documentation obligations that reference the insurance company by name. A true white-label platform must manage this requirement without exposing the insurer’s brand to the end customer in ways that break the white-label experience. This requires careful configuration of regulatory disclosure presentation — meeting the regulatory requirement while preserving the partner’s branded experience.

Why Most Platforms Fall Short at Scale

Many platforms deliver acceptable white-label capability for a single distribution partner. The limitations become visible when an insurer scales to five, ten, or twenty partners simultaneously.

The core problem is that most platforms implement white-label as a customisation layer on top of a single-brand core — rather than as a multi-partner architecture built into the platform from the ground up. As the number of partners grows, the customisation layer becomes increasingly complex to maintain, and changes to the underlying platform risk breaking partner-specific configurations.

| Surface white-label (customisation layer) | True white-label (partner architecture) |

|---|---|

| Logo and colour applied to shared templates | Full brand configuration per partner, automated |

| Manual document customisation per partner | Document generation engine with partner-level brand rules |

| Insurer references visible in API responses | Partner-specific API schemas with no insurer references |

| Shared data environment with access controls | Full data isolation per partner by architecture |

| Breaks at scale — 10+ partners unsustainable | Scales linearly — each new partner is a configuration, not a build |

The distinction between these two models is not visible in a vendor demo with a single partner. It becomes visible when an insurer’s distribution team tries to onboard a fifteenth bank partner in a tenth market and discovers that each one requires a custom development sprint rather than a platform configuration.

What to Ask Vendors About White-Label Capability

Insurers evaluating platforms for white-label distribution should ask vendors the following specific questions:

- Can you show us the document generation system? How is partner branding applied — through a configuration interface or through template customisation by the IT team?

- What insurer-specific references appear in API responses? Can we see a sample API response for a policy issuance call, and show us where partner-specific configuration applies?

- How is partner data isolated? Is it by access controls within a shared database, or by architectural separation?

- How do you handle regulatory disclosure requirements that reference the insurer by name, while maintaining the partner’s white-label experience?

- What happens to our partner configurations when you release a platform update? Is there a regression risk?

- How many distribution partners are you currently managing on the platform? Can you provide a reference from an insurer managing ten or more partners simultaneously?

Vendors that can answer these questions with specificity and evidence have built genuine white-label capability into their platform architecture. Vendors that respond with generalities or defer to case-by-case discussions are likely operating at the surface customisation level.

How CLAPi© AffinitiQ Delivers Multi-Level White-Label Capability

CLAPi© AffinitiQ is built on a partner-architecture model that delivers white-label capability across all five levels described in this article. Partner configurations in AffinitiQ are first-class platform objects — not customisation layers applied to a shared insurer-centric core.

The platform’s document generation engine uses a brand-rule system that applies partner-specific branding — logo, colour scheme, typography, sender identity, document footers — automatically across all document types without manual template customisation per partner. Adding a new distribution partner’s branding is a configuration exercise, not a development project.

AffinitiQ’s API layer exposes partner-specific schemas that contain no insurer-specific references in customer-facing data. Partner data is architecturally isolated within AffinitiQ’s multi-tenant structure, meeting both contractual and regulatory data residency requirements.

EnoviQ’s implementation approach means that a new distribution partner can be fully configured on AffinitiQ — including complete white-label setup across all five levels — within the partner onboarding timeline of weeks, not months. As the insurer’s partner portfolio grows, each new partner is a configuration exercise on the same platform infrastructure.

FAQs

A white-label insurance platform is an insurance administration and distribution system that allows insurers to present their insurance products entirely under a distribution partner’s brand. True white-label requires configurability at the UI, document, API, data, and compliance levels.

Banks and fintechs distributing insurance to their customer base need the product to appear as their own offering — consistent with their brand, embedded in their digital experience, and presented without visible insurance company branding. Visible insurer branding breaks the embedded distribution experience and reduces conversion and retention rates.

Surface white-label applies a distribution partner’s logo and colour scheme to standard insurer templates. True white-label delivers full partner brand isolation across UI, documents, APIs, data, and regulatory compliance presentation. The distinction is irrelevant for a single partner but critical when an insurer is managing multiple distribution partners simultaneously.

AffinitiQ uses a partner-architecture model where each distribution partner’s configuration — branding, product access, commission structure, regulatory rules — is a first-class platform object. New partners are configured through the platform’s partner setup module rather than through custom development, allowing the insurer to manage large and growing partner portfolios without linear increases in IT overhead.

Yes. AffinitiQ’s multi-tenant architecture provides architectural data isolation per distribution partner, supporting contractual data separation requirements between partners and market-specific data residency requirements across APAC jurisdictions.

Build a White-Label Insurance Distribution Operation That Scales

If your current platform is limiting your ability to offer genuine white-label experiences to distribution partners — or if scaling your partner portfolio is creating disproportionate IT overhead — CLAPi© AffinitiQ’s partner architecture is designed to solve these problems. Our team can demonstrate AffinitiQ’s white-label capability with a live partner configuration walkthrough.