Key Takeaways

- Bancassurance is the dominant insurance distribution channel in Asia Pacific — yet most insurers are running it on technology that was not designed for it.

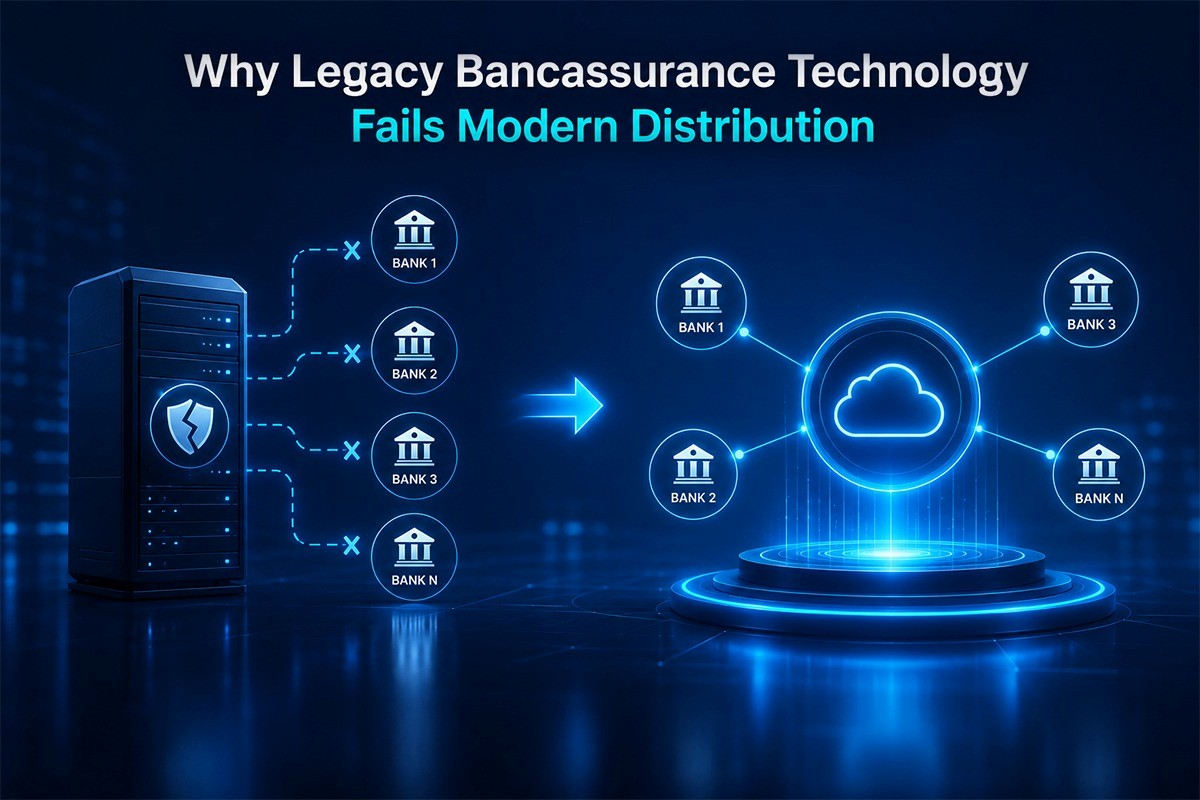

- Legacy bancassurance integrations are point-to-point, fragile, and take months to build for each new bank partner.

- A modern bancassurance technology platform must be API-first, white-label capable, real-time, and multi-bank scalable by design.

- Compliance across APAC markets — MAS, IRDAI, SFC, OJK — must be handled within the platform, not as a manual overlay.

- CLAPi© AffinitiQ is purpose-built for bancassurance distribution — enabling insurers to go live with new bank partners in weeks.

Bancassurance is the largest insurance distribution channel in most of Asia Pacific. In markets including Hong Kong, Singapore, Malaysia, Indonesia, and India, the majority of life and health insurance premiums collected each year flow through bank distribution partnerships. For many insurers, bancassurance is not just a channel — it is the channel.

Yet the technology infrastructure most insurers use to manage their bancassurance operations is fundamentally mismatched with the demands of modern bank distribution. Point-to-point integrations built for a single bank partner. White-label portals that are anything but white-label. Compliance workflows that rely on manual processes rather than platform-level controls.

The gap between what bancassurance distribution requires and what most insurer technology stacks deliver is one of the most consistently underinvested areas in insurance technology today. This article sets out six non-negotiable requirements that insurers should apply when evaluating or upgrading their bancassurance technology platform — and explains why most current solutions fail to meet them.

Why Legacy Bancassurance Technology Fails Modern Distribution

The traditional approach to bancassurance technology was integration-centric: build a bespoke connection between the insurer’s core system and each bank partner’s retail banking or CRM platform. Each integration was custom, took months to build, required ongoing maintenance by both parties, and broke every time either system was updated.

This model made a degree of sense when an insurer had one or two bancassurance partners and distribution volumes were manageable. It fails completely when an insurer is trying to operate bancassurance across multiple bank partners in multiple markets simultaneously.

| Legacy bancassurance technology | Modern bancassurance platform |

|---|---|

| Custom point-to-point integration per bank | Single API layer connects all bank partners |

| Months to onboard a new bank partner | Weeks to go live with new partner via standard API |

| Bank’s brand applied manually to documents | True white-label: full branding per partner, automated |

| Manual compliance checks per market | Platform-level regulatory controls per jurisdiction |

| Separate reporting per bank partner | Unified multi-partner analytics dashboard |

| Product changes require IT development | Product configuration via business rules engine |

The 6 Non-Negotiable Requirements for a Bancassurance Technology Platform

-

API-First Integration Architecture

The foundation of any modern bancassurance technology platform is an API-first integration architecture. This means the insurer’s core platform exposes all of its core functions — product quotation, policy issuance, mid-term amendments, claims initiation, and reporting — through open, documented APIs that bank partners can connect to through their own systems.

The alternative — building custom integrations per bank partner — is not viable at scale. An API-first architecture means that when a new bank partner is onboarded, the integration work is standardised and predictable. The bank connects to the same API layer that all other partners use, with partner-specific configurations applied at the platform level rather than through custom code.

Insurers evaluating a bancassurance platform should ask vendors directly: is the API layer built into the core platform, or is it a custom integration layer built on top of a monolithic system? The answer determines whether the platform can scale to multiple bank partners or will require disproportionate IT investment for each new relationship.

-

True White-Label Capability

White-label capability in bancassurance means that the insurance product and distribution experience presented to the bank’s customers appears to be entirely the bank’s own — the insurer’s branding is invisible. The bank’s name, logo, colour scheme, and tone appear on every customer touchpoint: proposal forms, policy certificates, renewal notices, claims correspondence.

Most platforms that claim white-label capability only offer logo and colour customisation on standard templates. Advanced white-label capability enables partner-level configuration of customer-facing journeys, documents, and interfaces, while still retaining mandatory insurer disclosures and compliance-required insurer elements where necessary.

For bancassurance, this is not optional. Bank partners have invested heavily in their customer relationships and brand trust. An insurance product that looks and feels like an insurance company product rather than a bank product undermines the distribution relationship and reduces conversion rates.

-

Real-Time Policy Issuance

Bank customers expect immediate confirmation when they purchase a financial product. In retail banking, account opening, card issuance, and loan approvals are increasingly instant or near-instant processes. Bancassurance insurance needs to meet the same expectation.

A bancassurance technology platform must support real-time policy issuance: the ability to process an insurance application, perform underwriting checks, issue a policy number, and generate a certificate of insurance within seconds of the customer completing the purchase interaction in the bank’s interface.

This requires the insurer’s underwriting rules to be configured as automated decision logic within the platform — not as a manual process that requires insurer staff review before issuance. For standard bancassurance products (group credit life, mortgage protection, travel, personal accident), automated underwriting covering the vast majority of applications is both achievable and expected.

-

Multi-Partner, Multi-Product Management

An insurer with a mature bancassurance operation will typically have multiple bank partners, each distributing one or more insurance products. Managing this complexity — different products per partner, different commission structures, different regulatory requirements, different reporting formats — is operationally intensive without the right platform.

A genuinely capable bancassurance distribution platform must provide centralised multi-partner management: a single insurer-side interface from which all bank partnerships are administered, with partner-specific configurations (products, rates, commissions, documents, branding) managed independently within the same system.

This is the difference between an insurer’s bancassurance team managing five separate system environments for five bank partners and managing one platform with five partner configurations. The operational cost difference is substantial.

-

APAC Regulatory Compliance Built In

Bancassurance is one of the most heavily regulated distribution channels in Asia Pacific. Regulatory frameworks governing bank-insurer partnerships vary significantly across markets — MAS guidelines in Singapore, IRDAI bancassurance regulations in India, SFC and IA requirements in Hong Kong, OJK regulations in Indonesia — and each has specific requirements around product approval, disclosure, sales process documentation, and mis-selling controls.

A bancassurance technology platform serving APAC markets must embed these regulatory requirements as platform-level controls, not manual process overlays. This means: mandatory disclosure presentation before purchase, configurable product eligibility rules, audit trails of all customer interactions, and reporting formats aligned to each jurisdiction’s supervisory requirements.

Insurers that rely on manual compliance processes in their bancassurance operations face both regulatory risk and operational inefficiency. Platform-level compliance controls eliminate the manual layer and provide a defensible audit trail for regulatory examination.

-

Partner Performance Analytics

Bancassurance distribution is ultimately a commercial relationship, and the insurer needs real-time visibility into how each bank partner is performing: premium volume, product mix, conversion rates, claims experience, and renewal rates — at the partner level, the branch level, and the individual product level.

A bank insurance distribution system that does not provide granular partner analytics forces the insurer to rely on manual data extracts and spreadsheet-based reporting — a process that is both slow and error-prone. Built-in partner analytics dashboards give the insurer’s distribution team the commercial intelligence they need to manage bank relationships actively and allocate resources to the highest-performing partnerships.

How CLAPi© AffinitiQ Meets These Requirements

CLAPi© AffinitiQ is EnoviQ’s purpose-built affinity and bancassurance distribution platform. It is designed from the ground up to address the six requirements outlined in this article, with bancassurance as a primary use case rather than an afterthought.

AffinitiQ’s API-first architecture allows new bank partners to be integrated using the same standard API layer, with partner-specific product and branding configurations applied without custom development. True white-label capability at the partner level means each bank’s distribution experience is fully branded to their identity.

The platform’s multi-partner management environment gives the insurer’s distribution team a single interface for all bancassurance relationships, with centralised analytics across the full partner portfolio. APAC regulatory compliance controls are built into the platform configuration layer, with jurisdiction-specific rule sets manageable without IT involvement.

EnoviQ’s implementation approach for AffinitiQ allows insurers to go live with a new bancassurance partner in weeks — a fraction of the time required by legacy integration approaches — giving insurers the speed to respond to new bank partnership opportunities without extended technology programmes.

FAQs

A bancassurance technology platform is an insurance administration and distribution system that enables insurers to manage their bank distribution partnerships — covering product configuration, real-time policy issuance, white-label customer experiences, commission management, and regulatory compliance — across multiple bank partners from a single system.

API-first architecture allows the insurer’s platform to connect with each bank partner’s systems through a standard, documented API rather than a custom point-to-point integration. This reduces the time and cost of onboarding new bank partners from months to weeks, and makes ongoing maintenance significantly simpler as either party’s systems evolve.

True white-label capability in bancassurance means the customer-facing experience can be extensively branded for the bank partner, including customised sales journeys, communication templates, and selected policy touchpoints. However, mandatory insurer disclosures, regulatory information, and insurer-operated interfaces remain visible where required for compliance and operational purposes. Platform-level white-label capability enables these configurations to be managed centrally for each bank partner without requiring manual customisation every time.

AffinitiQ provides a centralised multi-partner management environment where all bank partnerships are administered from a single insurer-side interface. Each partner has its own configuration — products, rates, commissions, branding, regulatory rules — managed independently within the same platform. Partner analytics dashboards provide real-time performance visibility across the full bancassurance portfolio.

EnoviQ’s standard implementation approach for new bancassurance partnerships on AffinitiQ targets go-live in weeks for standard product configurations. The exact timeline depends on the complexity of the bank partner’s integration requirements and the product set being distributed, but AffinitiQ’s API-first architecture and pre-built partner onboarding frameworks eliminate the months-long integration cycles typical of legacy approaches.

Build a Bancassurance Operation That Scales

If your current bancassurance technology is limiting your ability to onboard new bank partners quickly, manage multiple partnerships efficiently, or deliver a genuinely white-label experience, CLAPi© AffinitiQ is designed to solve exactly these problems. Our team can walk you through how AffinitiQ handles your specific bank partner and product requirements.