Key Takeaways

- Legacy employee benefits administration systems are failing insurers at the point where digital employer expectations meet analogue insurer operations.

- The core problem is architectural: most legacy systems were built for the insurer, not for the three-stakeholder model of insurer, employer, and employee.

- A modern employee benefits insurance software platform must connect all three stakeholders on a shared data model with real-time flows between them.

- CLAPi© EEQ is built on this three-stakeholder connected architecture, with self-service portals for all three parties.

Group employee benefits administration is at an inflection point in Asia Pacific. On one side, corporate employers are raising their expectations of what a digital benefits experience should look like — driven by the same digital-first experiences they encounter in every other area of their business operations. On the other side, most insurers are still administering those benefits on systems that were built before smartphones existed.

The gap between employer expectation and insurer capability is widening, and it is showing up in ways that matter commercially: slower policy issuance, more member data errors, more manual reconciliation, and an employer portal experience that bears no resemblance to the self-service digital tools employers use for HR, payroll, and finance.

This article examines why legacy employee benefits insurance software is failing modern insurers, what the new architecture looks like, and what a technology transition from old to new actually involves for a group benefits team.

The Architectural Problem with Legacy Benefits Systems

Most legacy group benefits administration systems were designed with one primary user in mind: the insurer’s own policy administration team. The employer was an external party that communicated with the insurer by email, spreadsheet, and phone. The employee was even further removed — largely invisible to the insurer’s system except as a row in a member data file.

This design reflected the operational reality of the time it was built. Employers communicated benefit changes via paper or later email. Employees claimed by submitting paper forms. The insurer’s administration team was the hub through which all information flowed.

The problem is that this architecture is structurally misaligned with how group benefits need to work in 2026. Employers expect to manage their benefits programme through a digital HR portal. Employees expect to access their benefits information, download certificates, and submit claims through a mobile interface. Brokers expect to manage their corporate accounts through a digital portal.

A legacy system built around the insurer as sole user cannot accommodate these expectations without extensive manual workarounds — and those workarounds are the primary driver of the administration cost that makes group benefits increasingly margin-constrained.

The Five Failure Modes of Legacy Group Benefits Administration

-

Manual Member Maintenance

Member additions, deletions, and data changes are communicated by employers via email or spreadsheet, manually entered by insurer administration staff, and periodically reconciled against payroll records. For an insurer managing hundreds of corporate schemes, this is the single largest source of administration cost and the primary driver of data errors.

-

Disconnected Renewal Process

Annual renewal requires the insurer’s team to manually rebuild each scheme from the current year’s claims experience, regenerate benefit schedules, recalculate premiums, and reissue documentation. The process is nearly as time-consuming as new business onboarding and provides little opportunity for the employer to self-serve.

-

No Real-Time Claims Visibility for Employers

Employers have limited visibility into the claims experience of their workforce until the insurer produces a periodic claims report — typically monthly or quarterly. This makes it impossible for employers to manage their benefits programme proactively or identify utilisation patterns that warrant benefit restructuring.

-

Siloed Data Across Products

An employer that purchases Group Health, Group Life, Group Travel and Group Personal Accident from the same insurer will often find that each product is administered on a separate system, with separate member records, separate certificates, and separate claims processes. From the employer’s perspective, this is a single relationship. From the insurer’s perspective, it is three separate administrative environments.

-

Poor Employee Experience

Employees typically have no direct relationship with the insurer’s administration system. They receive their insurance certificate once a year, access benefit information through HR, and submit claims by completing paper forms or uploading documents to a generic email address. This experience does not reflect the quality of the coverage being provided and contributes to low benefit utilisation and low employee satisfaction.

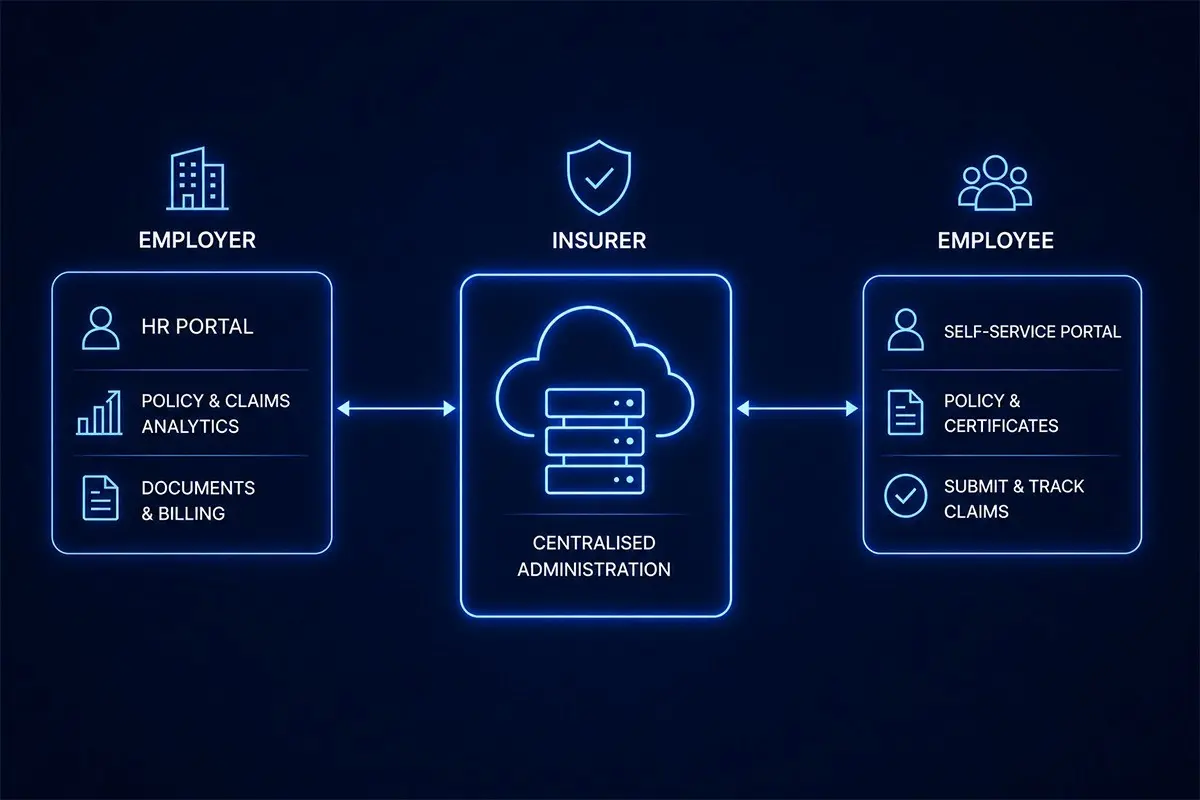

What the New Architecture Looks Like

The replacement architecture for legacy employee benefits insurance software is built on a fundamentally different model: three connected stakeholders — the insurer, the employer, and the employee — each accessing the same underlying data through purpose-built interfaces, with real-time data flows between them.

-

The Insurer Layer: Centralised Administration

The insurer’s administration team operates from a centralised scheme management environment where all corporate accounts — from enterprise clients to SMEs — are administered from a single platform. Policy administration, claims processing, premium billing, reinsurance, and document generation all operate within the same system. Member changes initiated by employers through their portal flow automatically into the insurer’s system without manual intervention.

-

The Employer Layer: HR Portal

The employer accesses the benefits programme through a digital HR Portal. Member additions and deletions are triggered automatically by HR Portal events rather than manual notifications. HR teams can access policy documents, premium statements, and claims analytics in real time. Renewal confirmations are completed digitally through the portal rather than through a manual back-and-forth with the insurer’s team.

-

The Employee Layer: Self-Service Benefits Portal

Employees access their benefits through a mobile-accessible self-service portal. They can view their current benefit entitlements, download their insurance certificates, submit claims with supporting document uploads, and track claim status in real time. The portal is branded to the employer’s identity and accessible without HR intermediation for routine benefit interactions.

How CLAPi© EEQ Implements This Architecture

CLAPi© EEQ is EnoviQ’s implementation of the three-stakeholder connected benefits architecture. The platform provides dedicated interfaces for all three stakeholders — insurer administration, employer HR Portal, and employee self-service portal — operating on a shared data model with real-time synchronisation between them.

The platform’s multi-tenant architecture allows a single EEQ deployment to serve an insurer’s full corporate portfolio — enterprise accounts, mid-market clients, and SME schemes — from the same infrastructure, with account-level configurations controlling the benefit structures, portal branding, and workflow rules for each employer client.

EnoviQ’s implementation approach allows insurers to go live on EEQ in weeks, with existing scheme data migrated from legacy systems through EEQ’s data migration tooling. The transition does not require a big-bang cutover — schemes can be migrated to EEQ progressively, allowing the insurer’s administration team to become familiar with the new system while managing the migration risk.

FAQs

Employee benefits insurance software is the administration platform that insurers use to manage group benefits programmes — covering policy issuance, member enrolment and maintenance, premium billing, claims processing, and reporting for corporate employer clients. Modern platforms connect the insurer, employer, and employee on a shared system with purpose-built interfaces for each stakeholder.

Legacy systems were designed for insurer-only administration and cannot support the three-stakeholder connected model that modern employers and employees expect. The specific failure modes — manual member maintenance, disconnected HR data, poor employer and employee digital experience — are driving increasing administration cost and employer dissatisfaction. Replacement is driven by both commercial pressure and competitive necessity.

EnoviQ’s implementation approach for EEQ supports progressive migration, allowing insurers to move schemes from legacy systems to EEQ over a managed timeline rather than in a single cutover. The exact migration timeline depends on the volume of schemes and the quality of data in the legacy system, but standard EEQ implementations achieve first scheme go-live within weeks of project initiation.

Yes. EEQ’s multi-tenant architecture supports corporate clients of all sizes on the same platform deployment, with account-level configuration controlling the benefit structures, portal branding, and workflow rules for each employer. Enterprise accounts with complex benefit structures and HR integration requirements are managed alongside SME schemes with standardised plan tiers on the same underlying system.

Modernise Your Group Benefits Administration

If your current employee benefits administration system is driving increasing cost, employer dissatisfaction, or operational complexity, CLAPi© EEQ is built to address these problems directly. Our team can walk you through EEQ’s three-stakeholder connected architecture and what a migration from your current system would look like.

Request a demo at enoviq.com/platform/employee-employer-platform